Right of Withdrawal

This article analyses the MiCA Offer to the Public (OTPC) process for Title II tokens. All regulatory references are to MiCA (Regulation (EU) 2023/1114) unless noted otherwise. This content is for informational purposes only and does not constitute legal, financial, investment, or professional advice. Cairn's Point is not liable for decisions made based on this information. Consumption of this material does not create a client relationship with Cairn’s Point. Always consult a qualified professional.

We often hear that initial coin offerings (ICOs) under the Markets in Crypto-Assets Regulation (MiCA) would require giving participants a 14 day period to withdraw from the ICO. This misconception probably stems from a misinterpretation of MiCA under certain offer characteristics and conflation of traditional consumer protection rules in distance contracts.

This misconception has allegedly led to projects choosing to not make their ICOs – or, more formally, OTPC – available to the public in the EU due to timing issues where the projects are looking to make their token available for trading immediately or soon after the conclusion of the subscription period of the OTPC. This has led some practitioners to believe that a EU OTPC would constitute a “free call option”, as the participant could receive a guaranteed refund within 14 days if the token price fell on secondary markets or sell the token if its secondary market price appreciated.

The relevant regulatory context is found in Article 13 which discusses the “Right of Withdrawal”. The statement that leads readers with a cursory understanding to believe in the misconception is the following in the first paragraph:

“Retail holders shall have a period of 14 calendar days within which to withdraw from their agreement to purchase … tokens without incurring any fees or costs and without being required to give reasons.”

The fifth paragraph clarifies that the last possible time to exercise the right of withdrawal is when the subscription period of an OTPC with a limited time window closes:

“Where offerors have set a time limit on their offer to the public … the right of withdrawal shall not be exercised after the end of the subscription period.”

In light of this paragraph, it is evident that an OTPC process which has a clearly defined subscription period would not incur refund processing after the end of the subscription period.

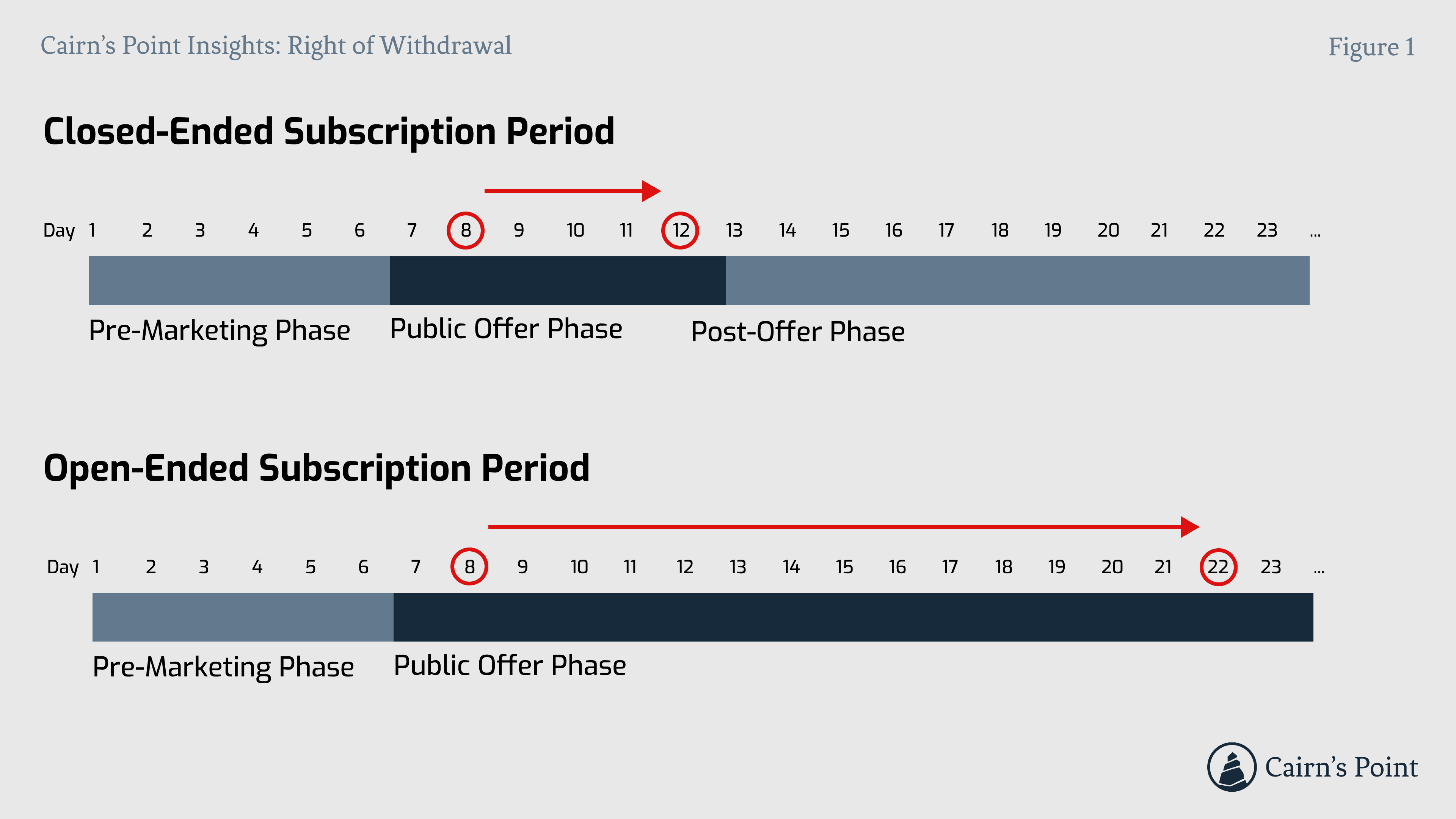

Let’s consider two examples of OTPC processes, one with a closed-ended subscription period and one with an open-ended subscription period compliant with 4(6):

Figure 1: Right of Withdrawal in a Closed-Ended vs Open-Ended OTPC Subscription Period

When the subscription period is closed-ended, the right to withdraw from participating in the subscription ends when the subscription period closes. As illustrated in Figure 1, if a retail holder commits to the public offer on day eight and the public offer subscription period ends on day 12, the last day they can withdraw from the offer is day 12.

For open-ended subscription periods where tokens are sold continuously without a pre-determined end date, the retail holder that commits on day eight would have the right to withdraw up until and including day 22.

The core distinction is the subscription period type; in limited time offers, the retail holders cannot exercise their right to withdraw after the subscription has closed. As per Figure 1, the token issuer could make their token available on the secondary market already on day 13 without any adverse impacts from retail holders exercising their right to withdraw.

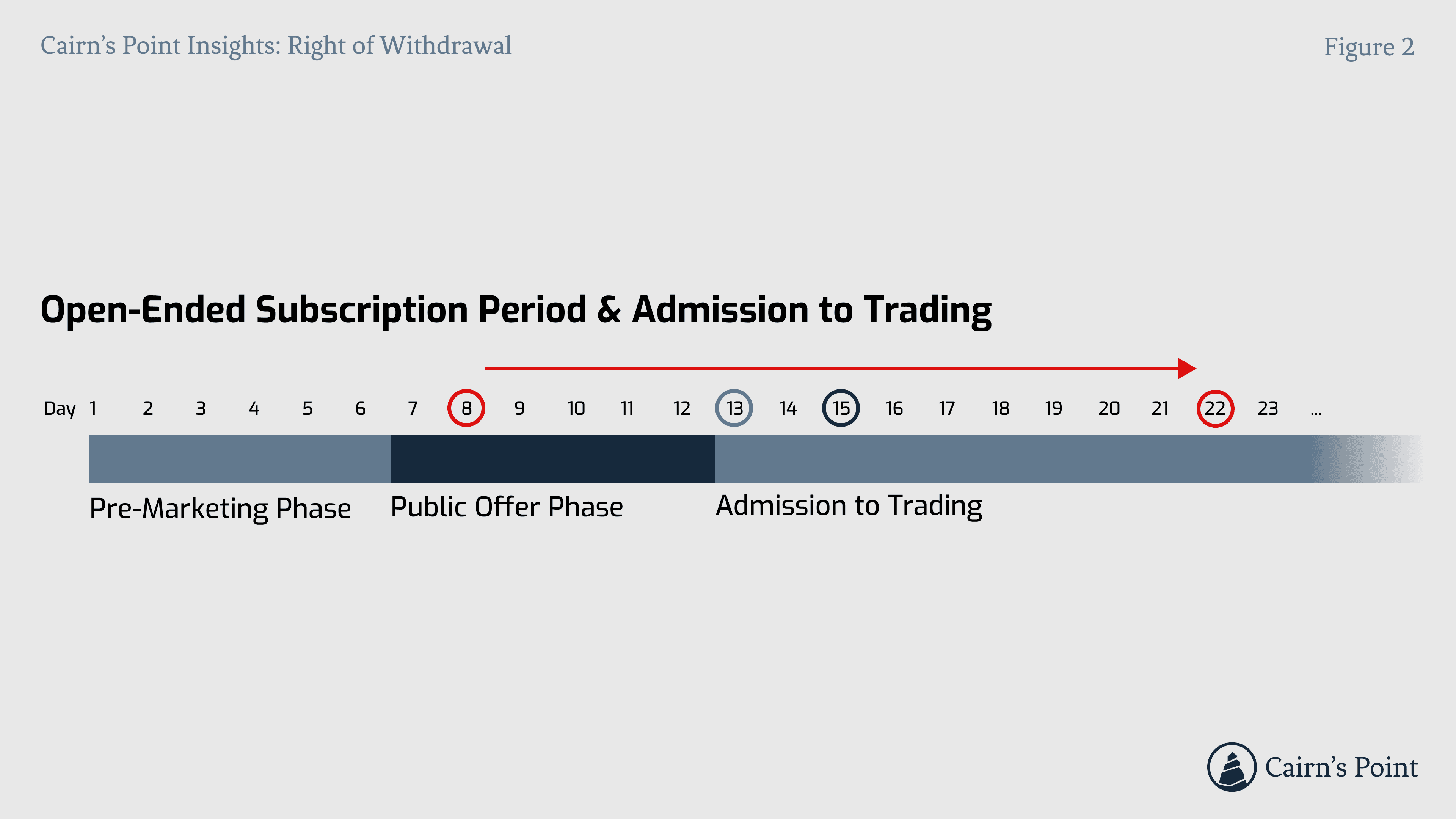

An additional important consideration is of that discussed in paragraph 4 of article 13; if the crypto-asset that is being offered for sale in the OTPC process is already admitted to trading – i.e. it is actively traded on an authorised venue under an ATTR white paper – at the time of purchase by the retail holder, the right of withdrawal does not apply. Therefore, even in the case of an open-ended offer, the retail holder would forfeit the right to withdraw if the token was made available in trading before the retail user’s purchase.

Figure 2: Right of Withdrawal in an Open-Ended OTPC Subscription when the Crypto-Asset is Admitted to Trading

In practice, as illustrated in Figure 2, a retail holder subscribing on day 8 would be able to withdraw until and including on day 22. However, if the asset was admitted to trading on day 13, a retail holder subscribing on day 15 would not have a right to withdraw.

In case where redemptions must be honoured, offerors should note that MiCA does require redemptions to be processed without undue delay and that the reimbursement should be generally carried using the same means of payment that the retail holder used for the initial transaction. For example, refunds for an OTPC raised in Ether on the Ethereum L1 should be processed without undue delay using Ether refunded to the wallet the retail holder used to subscribe to the OTPC with.

A common mistake that we see in OTPC offerings is that retail holders are not granted the full redemption rights due to them by regulation. The most common mistake is charging gas fees from the retail holder for subscription and redemption, when they should also be fully reimbursed unless properly structured.

In conclusion, under certain circumstances – arguably under the most common ICO models as of today – MiCA ICOs do not require a 14 day money back guarantee.